At MitonOptimal we take asset allocation (AA) very seriously, taking into consideration both Strategic AA (3-7 years) and Tactical AA within the various asset classes. This quarterly piece provides insight into our short term tactical calls on a 12-month view (reviewed quarterly) and as such may diverge from our long term strategic AA views. We review our strategic AA bi-annually as we believe this is prudent practice, in a world dominated by debt de-leveraging, central bank and political interference.

| Index | Q1-2024 | Q4-2023 |

| FTSE/JSE All Share | -2.25 | 6.92 |

| FTSE/JSE SA Listed Property |

3.85 |

16.37 |

| FTSE/JSE All Bond | -1.80 | 8.11 |

| FTSE/JSE ALB 1-3 Yr | 0.81 | 4.11 |

| Allan Gray Money Market | 2.20 | 2.20 |

| STeFI Composite | 2.06 | 2.09 |

| MSCI World | 12.74 | 8.15 |

| MSCI EM | 6.00 | 4.70 |

| S&P 500 | 14.35 | 8.29 |

| S&P Global REIT | 2.60 | 12.41 |

| GinsGlobal Global Bond Index | 0.23 | 4.58 |

| Bloomberg Commodity | 5.82 | -7.42 |

| USD Money Market | 4.85 | -1.66 |

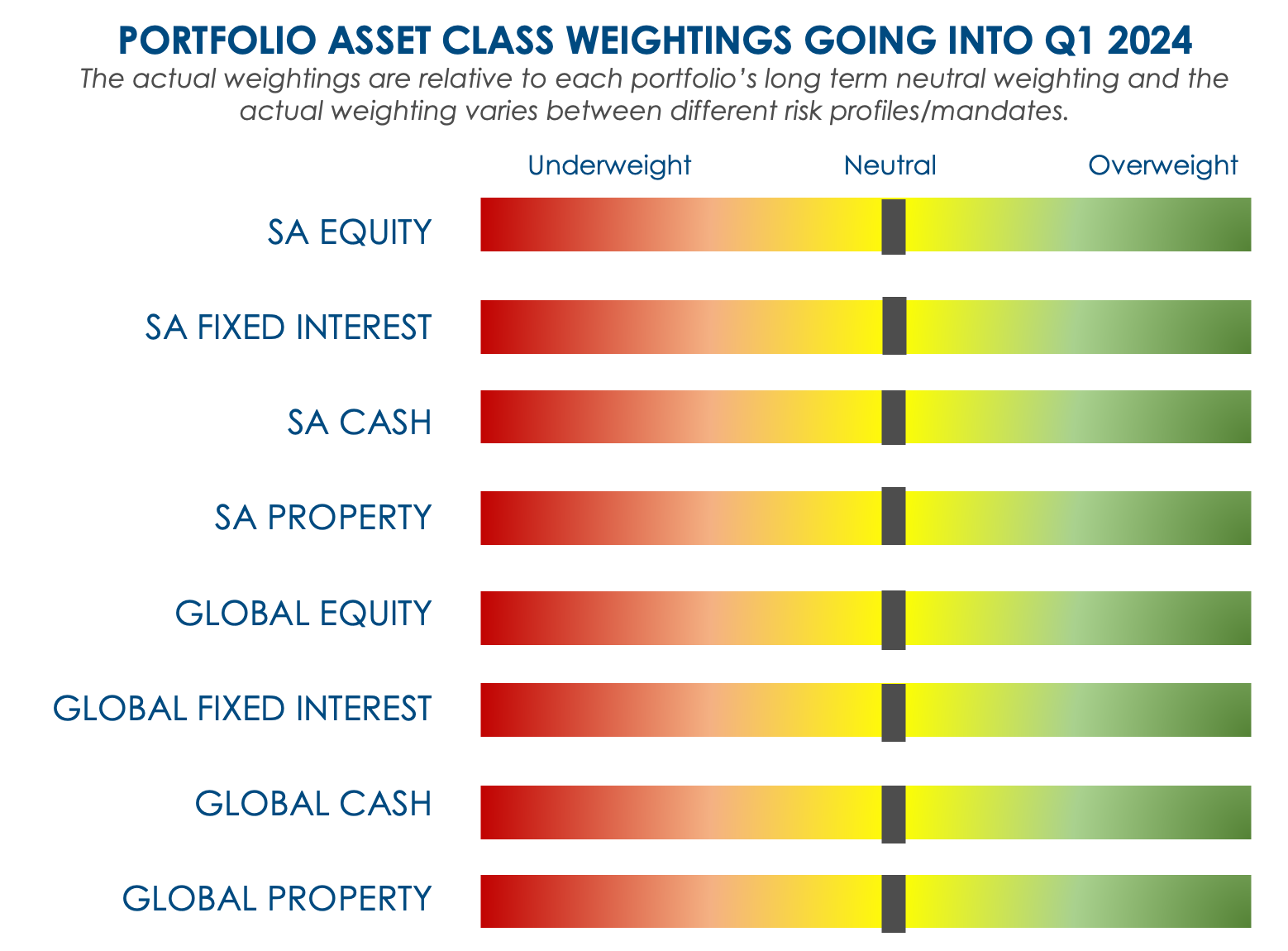

SA EQUITY

NEUTRAL – UNDERPERFORMED

Although SA equity did relatively well over the last month (3.23%), the asset class ends the quarter in the red (-2.25%). Despite the resurgence in the resources sector (15.36% last month and 0.82% for the quarter) the index was pulled down by pressures in the financial sector ( -3.49% for the month and -7.08% the quarter). Most of the risk-on behavior was because of the dovish nature of Central Banks.

It was mostly foreign disinvestment that was behind the downturn during the first two months of the year. Contentious elections looming, loadshedding still having an effect on business productivity and the relative strength of offshore assets (specifically S&P 500) were the major influences for this. Economic growth is also not helping, with GDP growth at 0.6% YoY for 2023 and the forecast for 2024 also around 1%.

On the opposite side of the spectrum, valuations for SA stocks are at the lowest levels they’ve been at in a long time. Many market participants see great value in this space but caution that it does come with quite a bit of risk.

We started the quarter in a neutral position and remained there for the entire quarter. There was minimal data to spark a move either way and with the uptick in the sector over the last month, we stick to the neutral stance. Our gaze is firmly set on the elections, and we will be monitoring closely what transpires pre- and post the 29th of May.

SA LISTED PROPERTY

NEUTRAL – OUTPERFORMED

The SA Listed Property sector performed well during Q1 of 2024 (3.5%) coming off the back of some stellar performance in December 2023. This was mostly because of the perception that interest rate cuts were on the cards and that federal bankers globally were close to pulling the trigger. In March, however, it was clear that the cuts were probably not as close or as severe as the market previously expected.

We moved to neutral in SA Property at the end of November and kept the neutral allocation throughout the quarter. This helped our portfolios on a relative basis as most of our peers remained underweight the asset class. We are keeping our neutral allocation going into Q2 and will revise once the cutting cycle begins.

SA FIXED INTEREST

NEUTRAL – UNDERPERFORMED

Unlike SA Listed Property, domestic bonds had a more difficult time during Q1 2024, returning -1.8%. There was a general preference for shorter dated bonds versus the ALBI. This coupled with the market reducing its expectation for rate cuts in SA this year is putting pressure on longer-duration maturities. The election that’s taking place on the 29th of May is also going to be a market mover and investors (especially foreign investors) are seeing too many uncertainties to be investing in the asset class at the moment.

We were neutral on the asset class during the quarter and remain there for Q2. The elections could cause us to move either way (overweight or underweight) during the next few months, but the future is just too uncertain at the moment to make any drastic calls.

SA CASH

NEUTRAL – NEUTRAL PERFORMANCE

We are neutral cash to keep our options open over the next few months and to be able to react quickly to changing market conditions.

GLOBAL EQUITIES

NEUTRAL – OUTPERFORMED

Global equities continued their outperformance over the other asset classes in Q1 2024. The MSCI World Index returned 12.74% in ZAR terms and was the best of the asset classes of the quarter. After our Strategic Asset Allocation meeting in November 2023, we preferred global equities over local equities, but remained neutral on our global equity allocation throughout the first quarter.

Our portfolios did well because of our short-term views and going favourably into global equities. The landscape going forward is more uncertain, though, with debt at extremely high levels and inflation looking stickier than the market anticipated three months ago. Also, many other countries are also having elections this year making the task of forecasting market conditions extremely difficult.

We remain neutral global equities, although we feel that this could change in the next 6 to 12 months as rate hiking cycles end and the central banks and governments become focused on growth rather than fighting inflation. We also remain biased towards global equities versus local equities, but without diverging much for the market allocation towards developed markets versus emerging markets.

GLOBAL PROPERTY

NEUTRAL – NEUTRAL PERFORMANCE

Global property (2.6% for Q1 2024) had a more difficult time and underperformed versus Global equities and SA Listed Property. Headwinds came in the form of potentially reduced rate cuts, higher debt levels and some pressures of Covid lockdowns still evident.

Our sector allocations also still hold, as we are focused on sectors such as warehousing, storage, data centers and infrastructure. We could be adding more to property if we feel an overweight allocation is warranted and prices revert to the longer-term average. We remain neutral with the possibility of going overweight if fundamentals turn in favour of this asset class.

GLOBAL FIXED INTEREST

NEUTRAL – UNDERPERFORMED

Global bonds struggled over the last month (0.12% in USD) as well as over the last quarter (-3.2% in USD). As discussed in the previous paragraphs, the revision of rate cuts and the expectation of rates staying higher for longer, had a negative effect on prevailing yields and caused the asset class to underperform.

We were neutral the asset class for most of the quarter, sticking to our strategic asset allocation calls. This might change going into the various elections and seeing how the market reacts to risk-on (or risk-off) scenarios playing out.

GLOBAL CASH

NEUTRAL – OUTPERFORMED

As with local cash exposure, the global cash allocation is used as either a risk mitigator or as a place holder for future deployment into risk opportunities. We moved to neutral exposure in Q4 and remained there for the duration of the first quarter in 2024.

With market conditions rather fluid, we remain neutral on the asset class with the possibility to deploy into risk assets if and when a risk-on signal appears.

All data sourced from Morningstar

DOWNLOAD: QUARTERLY MARKET INSIGHTS: Q1 2024

Jacques de Kock

Quantitative Analyst & Portfolio Manager

The content of this article is for information purposes only and does not constitute an offer or invitation to any person. The opinions expressed are subject to change and are not to be interpreted as investment advice. You should consult an adviser who will be able to provide appropriate advice that is based on your specific needs and circumstances. The information and opinions contained herein have been compiled or arrived at from sources believed to be reliable and given in good faith, but no representation is made as to their accuracy, completeness or correctness. MitonOptimal South Africa (Pty) Limited is an Authorised Financial Services Provider Licence No. 28160, regulated by the Financial Sector Conduct Authority (FSCA) – Registration No. 2005/032750/07.MitonOptimal Portfolio Management (Pty) Limited is an Authorised Financial Services Provider Licence No. 734, regulated by the FSCA – Registration No. 2000/000717/07.