At MitonOptimal we take asset allocation (AA) very seriously, taking into consideration both Strategic AA (3-7 years) and Tactical AA within the various asset classes. This quarterly piece provides insight into our short term tactical calls on a 12-month view (reviewed quarterly) and as such may diverge from our long term strategic AA views. We review our strategic AA bi-annually as we believe this is prudent practice, in a world dominated by debt de-leveraging, central bank and political interference.

| Index | Q4-2024 | Q3-2024 |

| FTSE/JSE All Share | -2.13 | 15.91 |

| FTSE/JSE SA Listed Property | -0.83 | 30.04 |

| FTSE/JSE All Bond | 0.43 | 16.68 |

| FTSE/JSE ALB 1-3 Yr | 1.45 | 8.08 |

| Allan Gray Money Market | 2.10 | 6.73 |

| STeFI Composite | 2.01 | 6.33 |

| MSCI World | 9.33 | 12.00 |

| MSCI EM | 0.73 | 10.12 |

| S&P 500 | 12.03 | 14.68 |

| S&P Global REIT | -0.12 | 7.35 |

| GinsGlobal Global Bond Index | 2.51 | -4.38 |

| Bloomberg Commodity | 9.01 | -0.25 |

| USD Money Market | 10.83 | -1.91 |

Source: Morningstar in ZAR

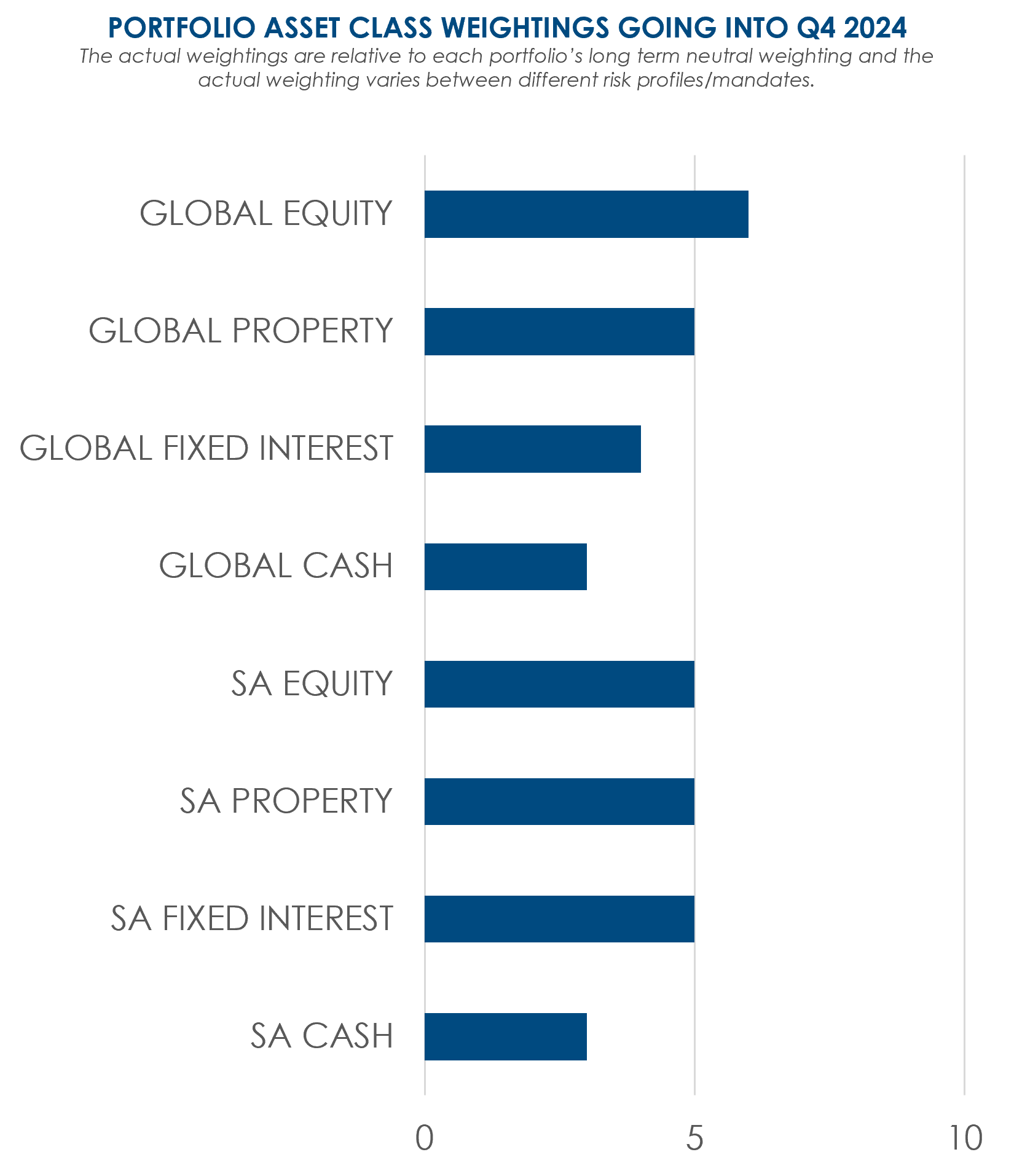

SA EQUITY

NEUTRAL – UNDERPERFORMED

South African equities, represented by the FTSE/JSE All Share Index, posted a return of -2.13% in ZAR terms during Q4 2024, underperforming other local and global asset classes. Despite local political stability and improving energy reliability, global macroeconomic pressures, including tighter liquidity conditions, declining commodity prices and a weakening Rand, weighed heavily on performance.

The financial sector, which is highly sensitive to interest rate dynamics, saw diminished investor interest as the South African Reserve Bank (SARB) held rates steady amidst rising global inflation concerns. Resource stocks, heavily reliant on global demand, faced additional challenges as commodity prices fell due to subdued Chinese growth. Industrials, including Naspers and Prosus, were negatively affected by volatility in global technology markets and currency headwinds.

Our neutral weighting in SA equities reflected a balanced view, recognising the local market’s risks amid global volatility. While domestic improvements remain encouraging, external headwinds limited upside potential.

SA LISTED PROPERTY

NEUTRAL – UNDERPERFORMED

The FTSE/JSE SA Listed Property Index declined by 0.83% in ZAR terms, reflecting a challenging environment for the property sector. The weakened likelihood of major rate cuts in 2025 dampened the prospects for this sector, although improved energy reliability and a stable inflationary environment provided some support. Our neutral weighting in this asset class ensured that portfolios were neither overly exposed to downside risks nor missed potential opportunities for income generation within high-quality property stocks.

SA FIXED INTEREST

NEUTRAL – NEUTRAL PERFORMANCE

South African bonds, as measured by the FTSE/JSE All Bond Index, returned 0.43% in ZAR terms for the quarter. Bond prices benefited from steady monetary policy by the SARB, which cut interest rates by only 25bps amid moderating inflation. Foreign inflows into local bonds also provided support as global investors sought higher yields amidst declining US Treasury rates.

However, concerns about fiscal sustainability, particularly around SOE debt obligations, tempered optimism. Our neutral allocation enabled us to participate in the stability offered by local fixed-income markets without taking on excessive risk.

SA CASH

UNDERWEIGHT – NEUTRAL PERFORMANCE

South African cash, represented by the STeFI Composite Index, returned 2.01% in ZAR terms during Q4 2024. While cash offered a safe haven amidst equity market volatility, its returns were overshadowed by higher-yielding opportunities in equities and bonds over the rest of the year.

Our underweight positioning reflected a deliberate choice to deploy capital in risk assets, which offered better prospects for growth and yield over the longer term and specifically during 2024. This aligns with our strategy to use cash selectively for liquidity and tactical positioning.

GLOBAL EQUITIES

OVERWEIGHT – OUTPERFORMED

Global equities, represented by the MSCI ACWI Index, delivered a strong 8.42% return in ZAR terms but -0.99% in USD terms. This divergence highlights the significant depreciation of the ZAR against the USD during the quarter. While local currency weakness inflated ZAR-denominated returns, global equities underperformed in USD due to lingering concerns over economic growth and mixed corporate earnings.

The US market, driven by a late-quarter rally in technology stocks, contributed significantly to global equity returns. However, Europe lagged amid continued recessionary pressures in Germany. Emerging markets showed mixed performance, with China benefiting from fiscal stimulus while facing ongoing property market concerns. Our overweight positioning allowed us to capture the ZAR-adjusted gains, aligning with our view of the relative attractiveness of global markets.

GLOBAL PROPERTY

NEUTRAL – UNDERPERFORMED

Global property, represented by the S&P Global REIT Index, delivered a return of -0.12% in ZAR terms and -8.78% in USD terms. Despite a weaker ZAR inflating local currency returns, global property markets underperformed due to ongoing challenges in the office and retail sectors, coupled with higher financing costs globally.

Key drivers of this underperformance included reduced leasing activity in developed markets, particularly in traditional office spaces, as hybrid work models became more entrenched. Meanwhile, segments such as logistics and industrial real estate showed resilience, benefiting from sustained e-commerce demand. Our neutral weighting reflects a balanced stance, recognizing both the opportunities in high-demand property sectors and the risks posed by valuation concerns and structural changes.

GLOBAL FIXED INTEREST

UNDERWEIGHT – NEUTRAL PERFORMANCE

Global fixed interest, as represented by the GinsGlobal Global Bond Index, returned 2.51% in ZAR terms and -6.39% in USD terms. This performance reflects the significant depreciation of the ZAR during the quarter, which boosted ZAR-adjusted returns for South African investors. However, bond markets globally faced headwinds as concerns over inflation and fiscal imbalances persisted.

Central banks in developed economies, including the US Federal Reserve and the European Central Bank, adopted more accommodative monetary policies, cutting interest rates to support slowing economies. Despite these measures, bond prices in USD terms remained under pressure. Our underweight allocation in global fixed interest was aligned with our view that risk-adjusted returns in other asset classes, such as equities, offered better prospects during the quarter.

GLOBAL CASH

UNDERWEIGHT – OUTPERFORMED

Global cash, represented by the OMG Money Market USD, delivered a notable return of 10.83% in ZAR terms and 1.22% in USD terms. This reflects the dual effect of strong ZAR depreciation and positive returns from short-duration money market instruments in USD.

Global cash provided stability during a volatile quarter, outperforming many other asset classes in ZAR terms. Our underweight positioning reflects a preference for growth-oriented and income-generating opportunities in equities and fixed income, though global cash remains a key component for managing liquidity and reducing portfolio risk.

- Overweight / Neutral / Underweight indicates the MitonOptimal asset allocation views

- Outperformed / Neutral / Underperformed indicates the asset class performance over the quarter

All data sourced from Morningstar

DOWNLOAD: QUARTERLY MARKET INSIGHTS: Q4 2024

Jacques de Kock

Quantitative Analyst & Portfolio Manager

The content of this article is for information purposes only and does not constitute an offer or invitation to any person. The opinions expressed are subject to change and are not to be interpreted as investment advice. You should consult an adviser who will be able to provide appropriate advice that is based on your specific needs and circumstances. The information and opinions contained herein have been compiled or arrived at from sources believed to be reliable and given in good faith, but no representation is made as to their accuracy, completeness or correctness. MitonOptimal South Africa (Pty) Limited is an Authorised Financial Services Provider Licence No. 28160, regulated by the Financial Sector Conduct Authority (FSCA) – Registration No. 2005/032750/07.MitonOptimal Portfolio Management (Pty) Limited is an Authorised Financial Services Provider Licence No. 734, regulated by the FSCA – Registration No. 2000/000717/07.